Using Your Pension to Fund Dental Implants in the UK (2026 Guide)

- UK pension rules give members age 55 and over significant flexibility in how they use their savings.

Whether you hold a Self-Invested Personal Pension (SIPP), a workplace defined contribution pension, or have a personal pension with a provider, the drawdown mechanism is the same: you access funds after the minimum pension age, and the tax treatment follows standard income tax rules.

Can I Use My Pension to Pay for Dental Implants?

Can UK patients use their pension to fund dental implants?

Yes, from age 55 (rising to 57 in 2028), UK pension holders can access their pension pot and use the funds for any purpose, including dental treatment. Up to 25% of the pension pot can typically be taken as a tax-free lump sum; additional withdrawals are taxed as income. There is no HMRC restriction on using pension funds for dental costs. Independent financial advice is strongly recommended before drawing down retirement savings.

UK pension rules give members age 55 and over significant flexibility in how they use their savings. Whether you hold a Self-Invested Personal Pension (SIPP), a workplace defined contribution pension, or have a personal pension with a provider, the drawdown mechanism is the same: you access funds after the minimum pension age, and the tax treatment follows standard income tax rules. Dental implants, like any medical or living cost, can be funded from pension income or a lump sum withdrawal.

This is distinct from Australia's "compassionate grounds" superannuation release, which has no direct equivalent in UK law. In the UK, pension access from age 55 is a standard right, not a special application process.

Questions about this procedure?

UK Pension Access: Key Facts

| Item | Detail |

|---|---|

| Minimum pension access age | 55 (rising to 57 in April 2028) |

| Tax-free lump sum | Up to 25% of the pension pot (lifetime limit applies) |

| Additional withdrawals | Taxed as income at your marginal rate |

| HMRC restriction on use | None, funds can be used for any purpose including dental costs |

| Application process | Via your pension provider, no HMRC application required |

| Pension types | SIPP, workplace defined contribution, personal pension, stakeholder |

| Defined benefit (final salary) | Different rules, check with scheme trustees before drawing |

| Financial advice | Strongly recommended, pension drawdown is irreversible |

Ready to discuss your options?

How Much Can You Access?

A pension pot of £100,000 allows:

- £25,000 tax-free lump sum (25%)

- Remaining £75,000 drawable as income, taxed at your marginal rate

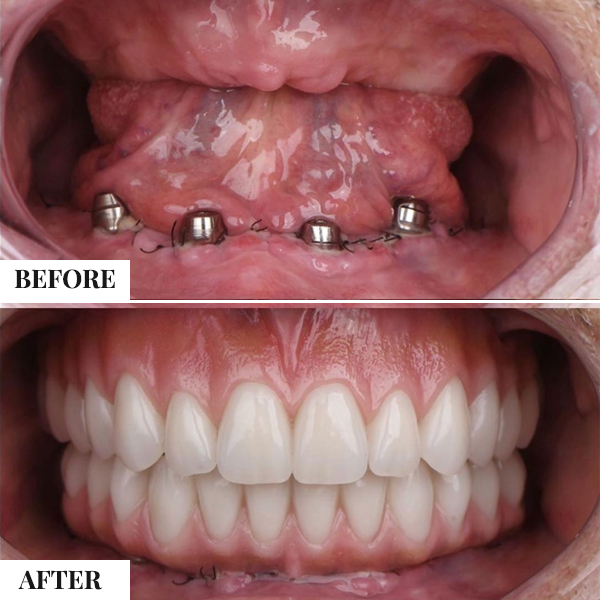

For full-arch implants at Stunning Dentistry (£10,000–£14,000 all-inclusive including travel), the tax-free component of most mid-size pension pots is sufficient to cover the entire treatment, leaving the taxable drawdown portion untouched.

Compared to funding the same treatment at UK prices (£40,000–£76,000), choosing dental tourism at Stunning Dentistry means drawing on significantly less of your pension pot.

Curious about costs and timelines?

Practical Steps for Pension-Funded Dental Treatment

There is no HMRC application process for standard pension drawdown. Funds are released by your pension provider once you reach the minimum access age and submit a withdrawal instruction.

| Step | Action |

|---|---|

| 1 | Confirm your pension type and current pot value with your provider |

| 2 | Seek independent financial advice (IFA), required for defined benefit transfers; strongly recommended for all pension drawdown decisions |

| 3 | Obtain a treatment plan and GBP-denominated quote from Stunning Dentistry (48-hour turnaround from scan upload) |

| 4 | Submit a drawdown request to your pension provider, standard processing: 5–15 business days |

| 5 | Receive funds. Book treatment. |

Want a personalised treatment plan?

Tax Implications

Large lump sum withdrawals can push you into a higher income tax band in the year of withdrawal. A phased drawdown strategy, spreading withdrawals across tax years, may reduce your overall tax liability. An IFA can model this for your specific situation.

| Age at Withdrawal | Tax Treatment |

|---|---|

| Under 55 (57 from 2028) | Typically not accessible (serious ill-health rules apply) |

| 55–74 | 25% tax-free; remainder taxed as income at marginal rate |

| 75+ | All withdrawals taxed as income; no further tax-free entitlement |

Questions about this procedure?

Using Pension Funds for Treatment in India

There is no HMRC or FCA restriction on using pension funds for overseas medical or dental treatment. Stunning Dentistry provides GBP-denominated quotes and payment receipts compatible with UK financial and tax documentation requirements. Most UK patients can fund their full treatment, including travel, accommodation, and the definitive prosthesis, using only the tax-free portion of a modest pension pot.

Ready to discuss your options?

People Also Ask

Can I access my pension early for dental implants?

Standard pension access begins at age 55 (57 from 2028). There is no special early-access scheme for dental treatment in UK law, unlike Australia's compassionate grounds superannuation release. Serious ill-health early access exists but applies to terminal illness, not dental conditions.

Is pension drawdown for dental implants taxed?

The first 25% of your pension pot is typically tax-free. Additional drawdowns are taxed as income at your marginal rate. Draw in the same tax year as other low-income periods to reduce your effective rate.

Do I need HMRC approval to use my pension for dental treatment?

No. Standard drawdown from a SIPP or workplace pension does not require HMRC approval, only a request to your pension provider. HMRC is involved only in the tax treatment of the withdrawal, which your provider handles automatically.

Can I use a workplace pension for dental implants?

Yes, from age 55 (57 from 2028) if the scheme rules permit flexible drawdown. Some workplace defined contribution schemes require you to transfer to a SIPP to access flexible drawdown. Check with your HR or pension scheme trustees.

Get GBP Treatment Quote → | Calculate Your Savings → | UK Insurance Guide →

*This page provides general information only and does not constitute financial advice. Consult a regulated independent financial adviser (IFA) before making pension drawdown decisions. Last updated: May 2026.*

Curious about costs and timelines?

Specialist-only treatment planning

- Remote file review before travel

- Evidence-led treatment checkpoints

No waiting list for eligible cases

- Remote file review before travel

- Evidence-led treatment checkpoints

Trip coordinated with care timeline

- Remote file review before travel

- Evidence-led treatment checkpoints

Our Partners

Why Us

See your new smile instantly!

This tool will help you understand potential structural and aesthetic changes before finalizing treatment decisions.